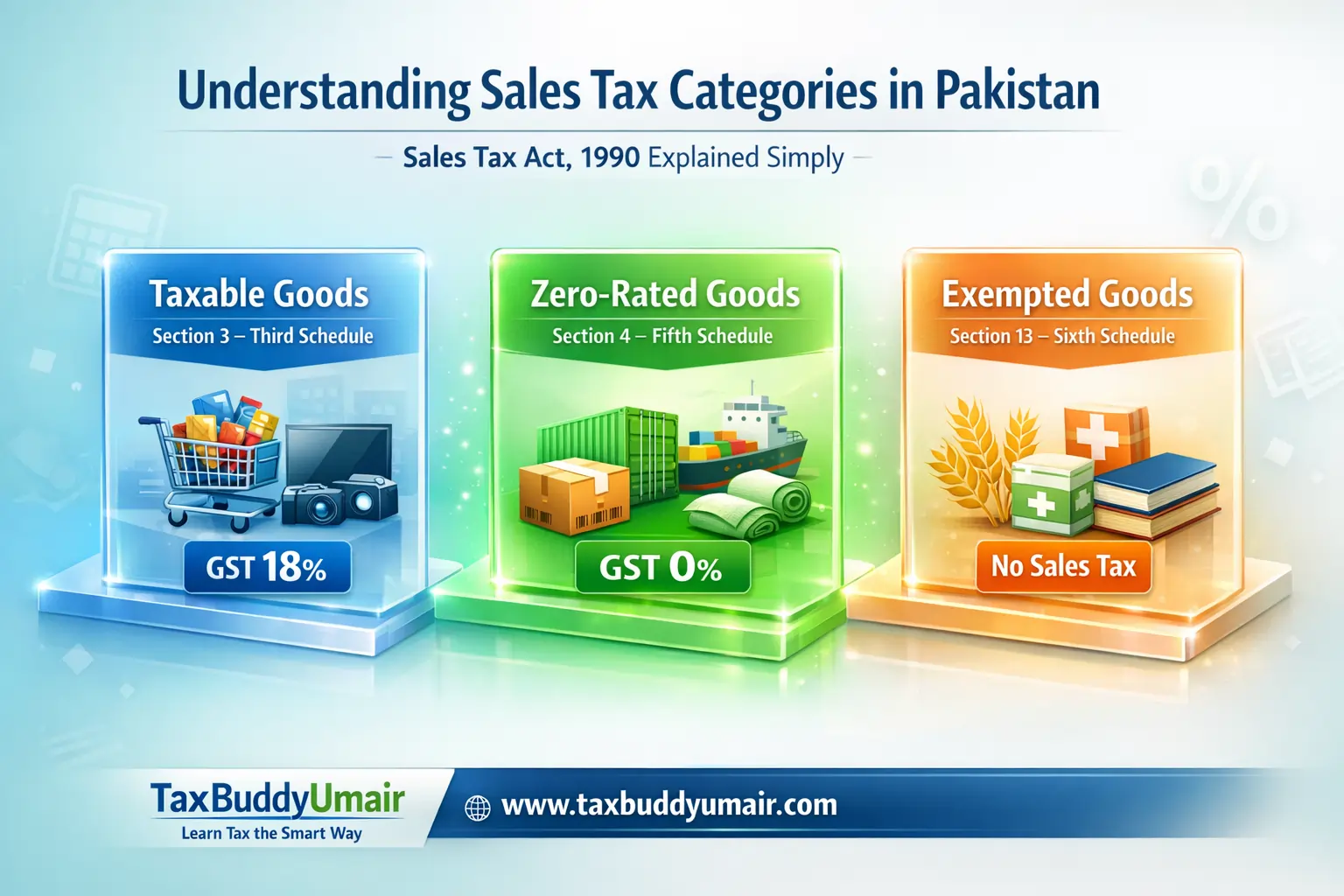

Types of Goods under the Sales Tax Act, 1990 in Pakistan

Understanding the classification of goods under the Sales Tax Act, 1990 is essential for business owners, exporters, tax consultants, and students in Pakistan. The Sale Tax Act, 1990 divides goods into three main categories: Taxable Goods, Zero-Rated Goods, and Exempted Goods. Each category has a different sales tax treatment and directly affects pricing, input tax adjustment, refund eligibility, and compliance requirements. Incorrect classification can lead to penalties, additional tax demands, or refund rejection.

1. Taxable Goods (Section 3 – Third Schedule)

Taxable goods are those on which General Sales Tax (GST) is charged at the standard rate of 18%. Most goods sold in Pakistan fall under this category. If you are a registered person making taxable supplies listed in third schedule, you must charge 18% GST on your sales. The input tax paid on your purchases can be adjusted against output tax. These transactions must be reported in your monthly sales tax return. If goods are not specifically listed as zero-rated or exempt, they are generally treated as taxable.

2. Zero-Rated Goods (Section 4 – Fifth Schedule)

Zero-rated goods are taxable supplies charged at 0% GST. This category is especially important for exporters. Although the tax rate is 0%, these goods are still considered taxable supplies under the Sales Tax Act, 1990. Zero-rated goods are mainly used by exporters. When exporters purchase raw materials, packing materials, or services, they usually pay 18% GST on those purchases. However, when they export the finished goods, they charge 0% GST.

The major advantage is that the input tax paid on purchases is refundable. For example, if an exporter buys raw material worth Rs. 1,000,000 and pays Rs. 180,000 as GST, and then exports the finished goods at 0% GST, the Rs. 180,000 becomes refundable. This refund system supports exporters, improves cash flow, and encourages foreign exchange earnings. It is important to understand that zero-rated goods are refundable, while exempted goods are not.

3. Exempted Goods (Section 13 – Sixth Schedule)

Exempted goods are completely free from sales tax. No GST is charged on their sale. Examples include basic food items, fresh fruits and vegetables, certain medicines, educational books, and specific agricultural products. However, the key point is that input tax adjustment is not allowed on exempt goods. If a business pays GST on purchases related to exempt goods, that tax cannot be claimed as Input Tax or refunded. This increases the cost for businesses dealing only in exempt supplies.

Key Differences Between Taxable, Zero Rate and Exempted Goods

- Taxable goods are charged at 18% GST and input tax adjustment is allowed.

- Zero-rated goods are charged at 0% GST and input tax is refundable, especially for exporters.

- Exempted goods have no GST, but input tax cannot be claimed or refunded.

💬 Comments 0

No comments yet. Be the first to share your thoughts!

✍️ Leave a Comment

Your comment will be reviewed before publishing. Please keep it relevant and respectful.