Capital Gain Tax Reduction 9A Second Schedule ITO-2001

Legal Reference 9A of Part III, Second Schedule – Income Tax Ordinance, 2001

50% Capital Gains Tax Reduction

Under 9A, Part III, Second Schedule – ITO, 2001

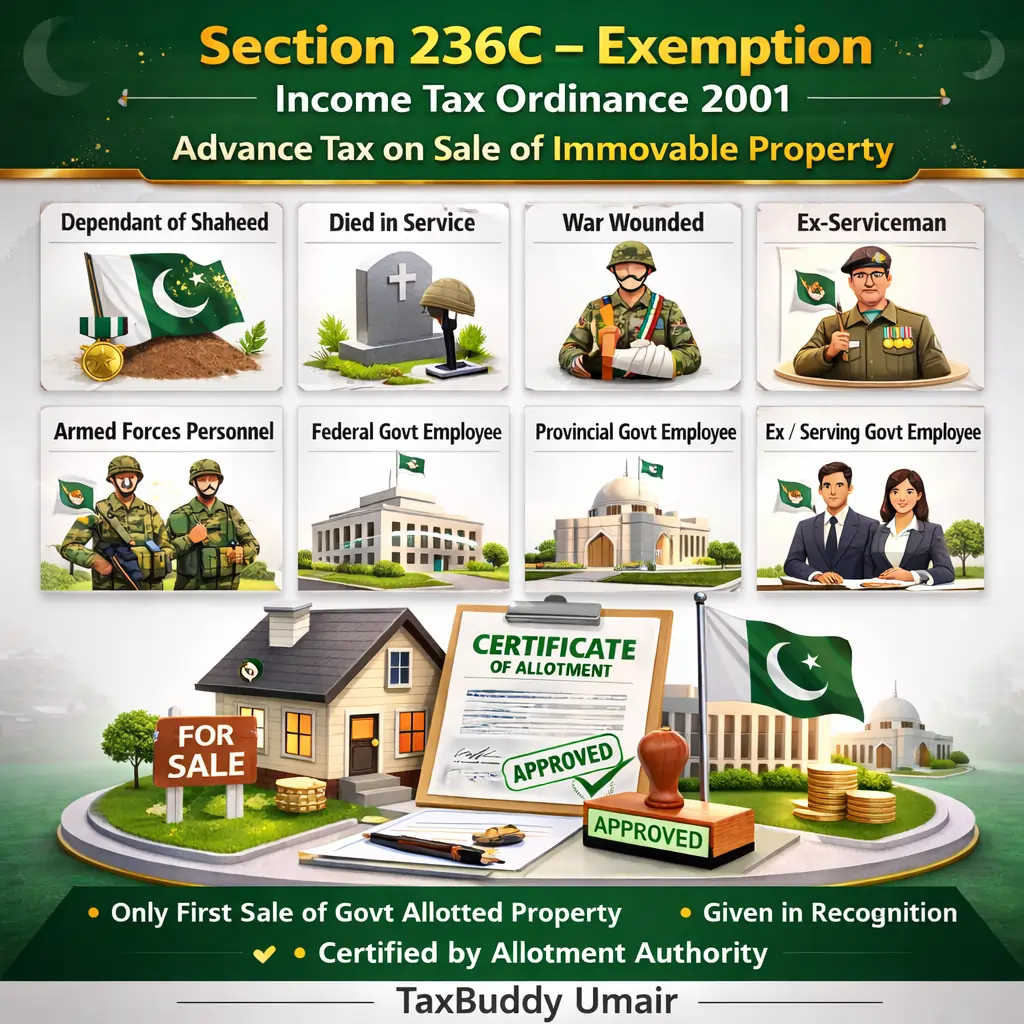

The Government of Pakistan provides significant tax relief to specific categories of individuals on the first sale of allotted immovable property. This relief is granted under 9A of Part III, Second Schedule of the Income Tax Ordinance, 2001.

If you are a government employee or a member of the Armed Forces, this provision can substantially reduce your Capital Gains Tax (CGT) liability. This provision allows a reduction in capital gains tax on the first disposal of certain allotted immovable properties.

Who Is Eligible?

The

tax reduction applies to the following categories:

- Ex-servicemen

- Serving Armed Forces personnel

- Former Federal Government

employees

- Current Federal Government

employees

- Former Provincial Government

employees

- Current Provincial Government

employees

What Type of Property Qualifies?

The

relief applies only if:

- The property is immovable

property

- The property was acquired or

allotted by the Government

- The property is being sold for

the first time

- The seller is the original

allottee

- Certification is obtained from

the allotment authority

If

these conditions are not fulfilled, the relief cannot be claimed.

50% Capital Gains Tax Reduction

On

the first sale of the allotted property, the taxpayer is entitled to a 50%

reduction in Capital Gains Tax.

Example:

- Capital Gain: Rs. 2,000,000

- Applicable Tax Rate: 15%

- Standard Tax: Rs. 300,000

After 50% Reduction: Tax Payable: Rs. 150,000

This results in a direct tax saving

of Rs. 150,000.

75% Tax Reduction After 3 Years

An

even greater benefit applies if the property is sold after three years from the

date of acquisition.

In

that case, the tax on capital gains is reduced by 75%.

Example (After 3 Years):

- Capital Gain: Rs. 2,000,000

- Standard Tax: Rs. 300,000

After 75% Reduction: Tax Payable: Rs. 75,000

This provides a total tax saving of

Rs. 225,000.

Important Conditions to Remember

Before

claiming this relief, ensure:

- You are the original allottee

- The sale is the first disposal

of the property

- The allotment authority

certifies your eligibility

- All documentation is properly

maintained

Incorrect claims may lead to penalties, disallowance of relief, or additional tax liability.