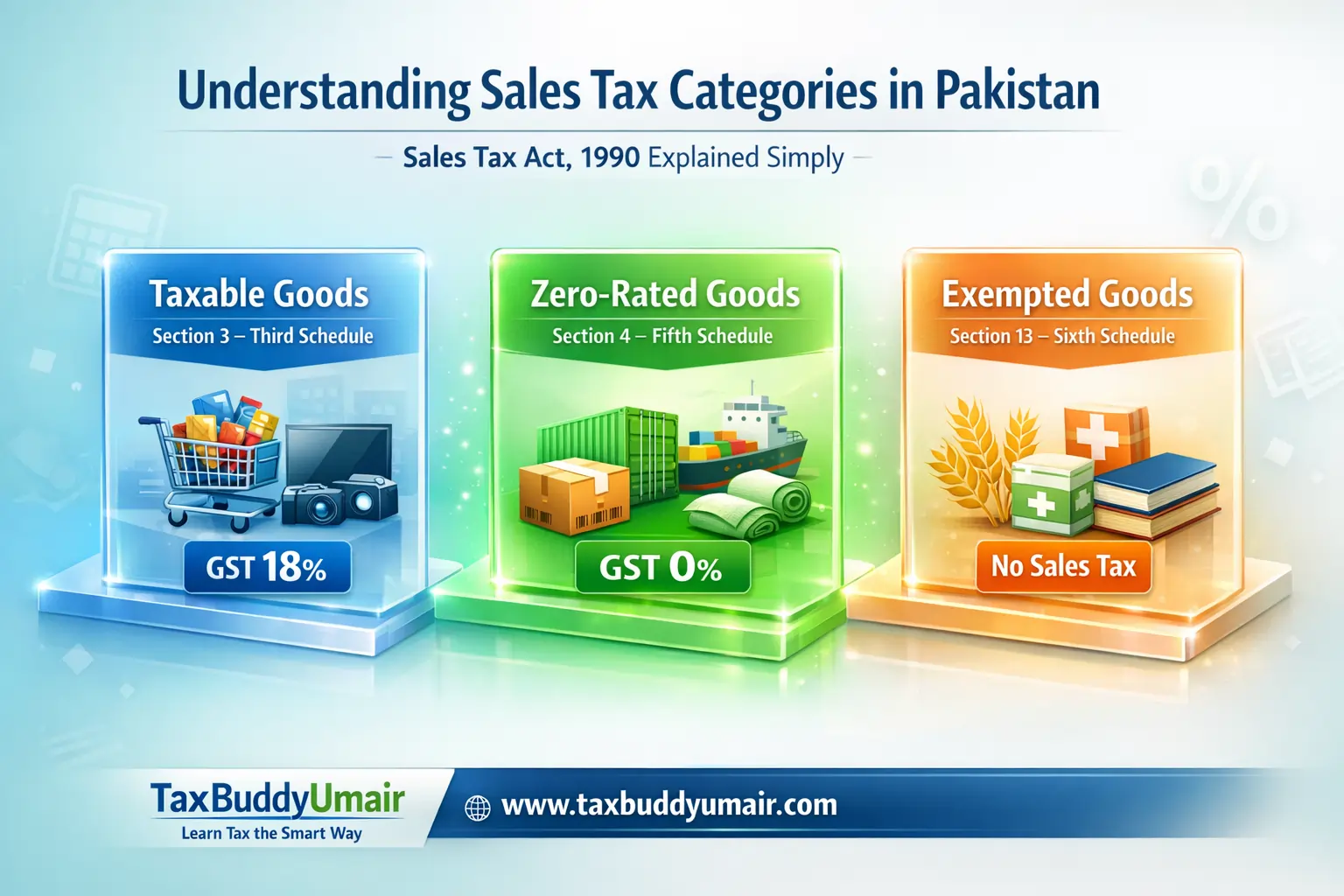

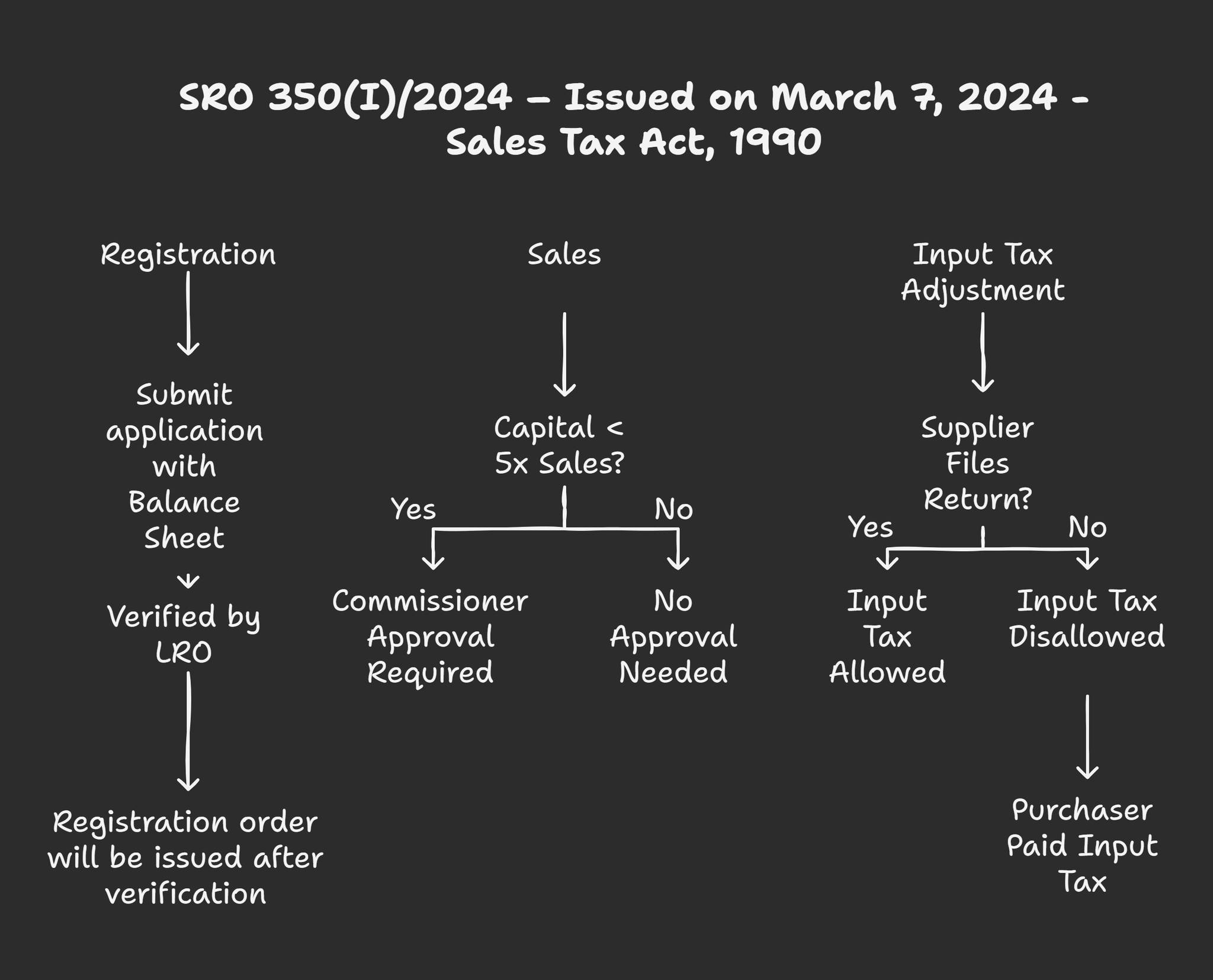

Essential Concepts Sales Tax Returns Pakistan

Essential Concepts to File Sales Tax Returns – Sales Tax Act, 1990 (Pakistan)

Understanding sales tax return filing is not just about filling numbers in a form. It requires a clear understanding of the core tax concepts defined under the Sales Tax Act, 1990. Many businesses struggle with return submission because they do not fully understand how Input Tax, Output Tax, Excess Input Tax, and Further Tax work in practice.

This article explains these four essential concepts in simple language with practical examples to help business owners, accountants, Income Tax Practitioner , Income Tax / Sales Tax Consultant and students master sales tax return filing in Pakistan.

1. Input Tax (18%) – Sales Tax Act, 1990

Input Tax is the sales tax paid on taxable purchases from registered suppliers. When you purchase taxable goods, the supplier charges 18% sales tax. This amount becomes your claimable input tax.

Example:

- Purchase Value: Rs. 100,000

- Sales Tax (18%): Rs. 18,000

- Input Tax = Rs. 18,000

2. Output Tax (18%) – Sales Tax Act, 1990

Output Tax is the sales tax charged when you sell taxable goods. You must charge 18% sales tax on taxable supplies at the time of sale. This amount becomes your claimable output tax.

Example:

- Sale Value: Rs. 150,000

- Sales Tax (18%): Rs. 27,000

- Output Tax = Rs. 27,000

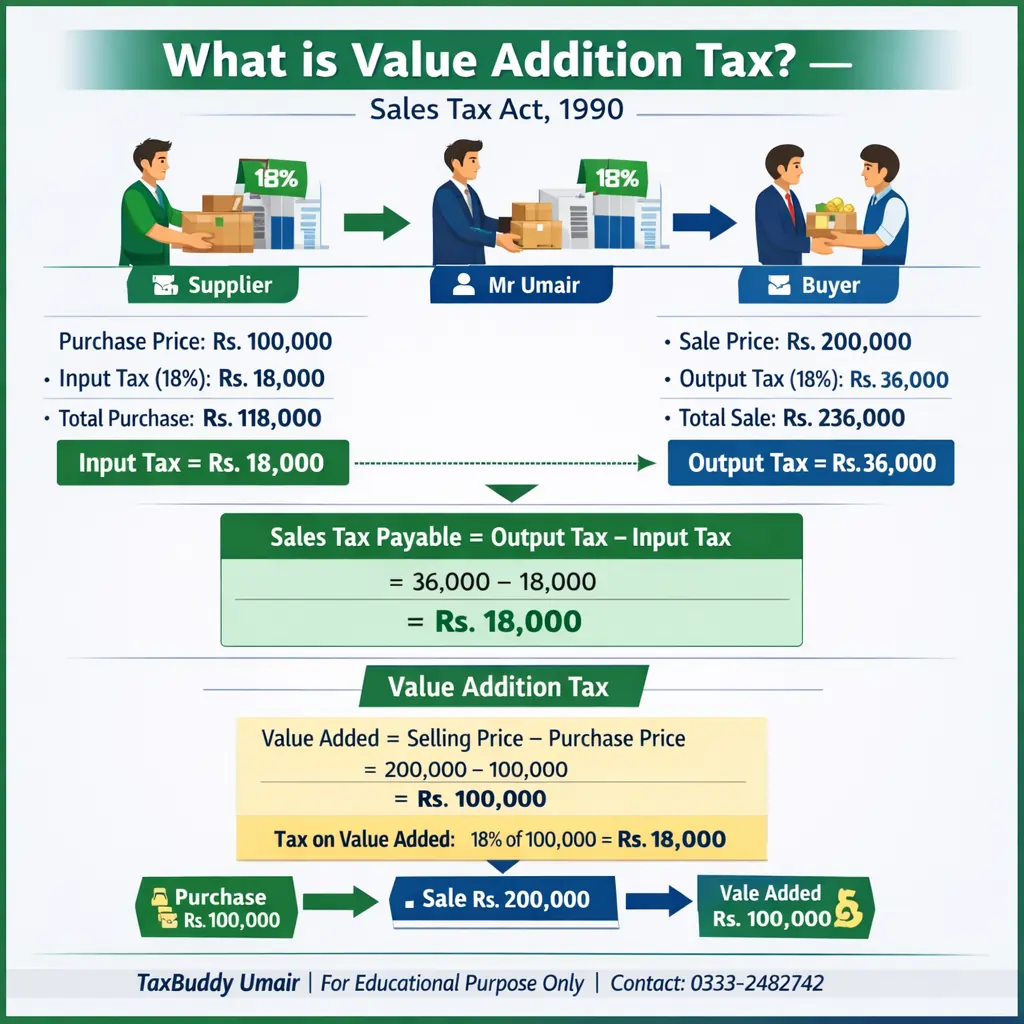

Sales Tax Payable Formula

Sales Tax Payable = Output Tax – Input Tax

Using the above examples:

- Output Tax = Rs. 27,000

- Input Tax = Rs. 18,000

- Net Tax Payable = Rs. 9,000

If Output Tax is higher → You pay the difference.

If Input Tax is higher → Excess is carried forward.

3. Excess Input Tax – Sales Tax Act, 1990

Excess Input Tax occurs when Input Tax exceeds Output Tax in a tax period.

Example:

- Input Tax: Rs. 30,000

- Output Tax: Rs. 25,000

- Excess Input Tax = Rs. 5,000

This amount is not refunded automatically. It is:

- Carried forward to the next month

- Adjusted against future output tax

4. Further Tax (4%) – Total Becomes 22%

Further Tax applies when a registered person makes taxable supplies to an unregistered person. If the buyer is unregistered, an additional 4% Further Tax must be charged.

So the total becomes:

18% + 4% = 22%

Example:

- Sale Value: Rs. 100,000

- Sales Tax (18%): Rs. 18,000

- Further Tax (4%): Rs. 4,000

- Total Tax = Rs. 22,000

- Total Invoice = Rs. 122,000

Final Thoughts : The Sales Tax Act, 1990 follows a structured mechanism: tax moves from supplier to business to customer, with adjustments made at each stage.

If you understand:

- Input Tax (18%)

- Output Tax (18%)

- Excess Input Tax

- Further Tax (4%)

Note : You understand the foundation of sales tax return filing. Accurate calculation, proper documentation, and monthly reconciliation ensure compliant and stress-free tax management.

Disclaimer

This content is for educational purposes only and does not constitute professional tax advice. Consult a qualified tax practitioner for case-specific guidance.