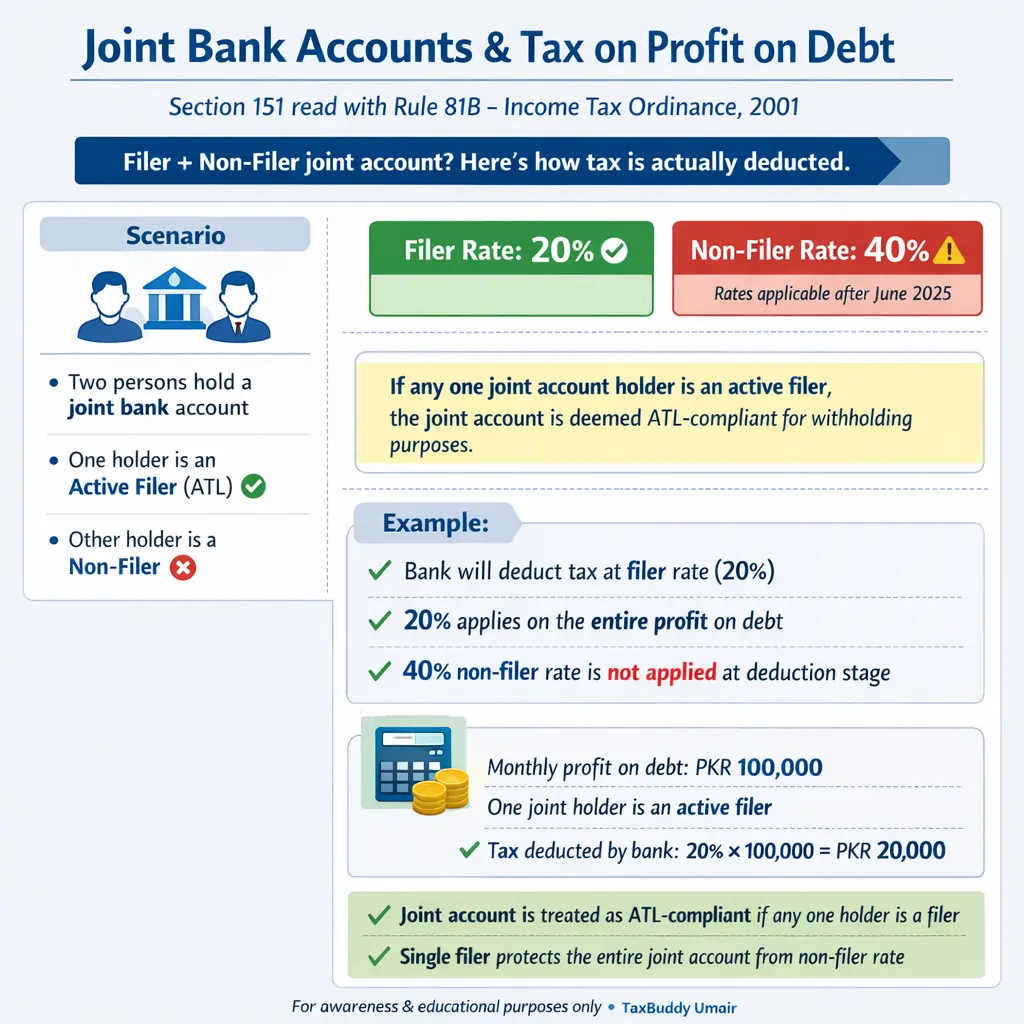

When Advance Tax on Sale or Transfer of Immovable Property Becomes Minimum Tax

Section 236C – Advance Tax on Sale or Transfer of Immovable Property - ITO, 2001

Under sub-section (2) of Section 236C, when someone sells or transfers an immovable property, a certain amount of tax is collected. This tax is usually adjustable—meaning it can be subtracted from the person’s total tax liability for the year.

However, there’s an exception:

If a person buys and sells the same property within the same tax year, then the tax collected or="#080809"> will be treated as the minimum tax. In this case, it cannot be adjusted or refunded, even if their actual tax liability is lower.

Example:

Mr. Umair buys a plot in July 2025 and sells it in December 2025 - same tax year.

At the time of sale, advance tax is collected under Section 236C.

Normally, this tax would be adjustable, but because Mr. Umair bought and sold the property within the same year, the tax is now treated as minimum tax means treated as Non Adjustable and non refundable.